Bulle du capital-risque

La faillite de la Silicon Valley Bank (SVB), la 16ème banque américaine et la 2ème faillite la plus importante de l’histoire des Etats-Unis, interpelle autant les marchés que la presse financière par sa rapidité et son ampleur.

Elle illustre à nos yeux une nouvelle étape dans la convergence du système macro-financier.

Ce billet s’intéresse à ce que nous pensons être les principes actifs, les mécanismes qui ont scellé le sort de SVB. Nous parcourons et réarrangeons quelque peu l’actualité financière le long des têtes de chapitres suivantes:

- Le modèle d’affaires de SVB

- Cash burn

- Run bancaire

- Effets de contagion : directs, carry, réglementaires

- Et maintenant ?

Nos propositions suivent en fin de billet. La convergence macro-financière s’est fortement accélérée depuis la fin de l’année 2021. Les failles de stabilité financière en sont une des manifestations privilégiées. Elles sont loin d’être terminées. La faillite de SVB puise dans le même vivier que la crise des Gilts anglais : des effets de levier considérables, une gestion assez créative des risques, des promesses d’interventions publiques illimitées – le nombre de fonds de PE ou de HFs qui les appellent de leurs vœux est invraisemblable ! – et des problèmes d’aléa moral dont le monde financier raffole.

La faillite de SBV marque sans doute la fin de la bulle du capital-risque tel que nous l’avons connue ces dernières années.

Par définition, le sujet est fondamentalement systémique.

Bonne lecture.

1. Silicon Valley Bank et son modèle d’affaires

(1) What was Silicon Valley Bank? Although it was not in the same league as, say, Goldman Sachs or J.P. Morgan Chase, Silicon Valley Bank, or SVB, punched above its weight during its 40-year history.

Based in Santa Clara, Calif., its clients included venture capital firms and startups, and it became a big player in the tech sector, successfully competing with bigger-name banks.

“They really developed a niche that was the envy of the banking space,” says Jared Shaw, a senior analyst at Wells Fargo. “They are able to provide all the products and services any of these sophisticated technology companies, as well as these sophisticated venture capital and private equity funds, would need.”

But it remained little known outside of tech circles — until this week.

Ces compagnies techno sophistiquées ainsi que leurs fonds de capital-risque méritent le détour. La faillite de SVB est en effet intimement liée au cycle des investissements en private equity, ou plutôt aux montagnes de liquidités versées par les investisseurs :

(2) In 2021, at the height of an investment boom in private technology companies, SVB received a flood of money. Companies receiving ever larger investments from venture funds ploughed the cash into the bank, which saw its deposits surge from $102bn to $189bn, leaving it awash in “excess liquidity”.

Searching for yield in an era of ultra-low interest rates, it ramped up investment in a $120bn portfolio of highly rated government-backed securities, $91bn of these in fixed-rate mortgage bonds carrying an average interest rate of just 1.64 per cent. While slightly higher than the meagre returns it could earn from short-term government debt, the investments locked the cash away for more than a decade and exposed it to losses if interest rates rose quickly.

When rates did rise sharply last year, the value of the portfolio fell by $15bn, an amount almost equal to SVB’s total capital. If it were forced to sell any of the bonds, it would risk becoming technically insolvent.

The investments represented a huge shift in strategy for SVB, which until 2018 had kept the vast majority of its excess cash in mortgage bonds maturing within one year, according to securities filings.

Nous revenons en fin de billet sur ce que nous pensons être l’élément central de cette faillite : une bulle des investissements dans les fonds de capital-risque et une érosion féroce des capitaux.

2. Le “cash burn” ou la sensibilité financière du modèle des startups technos

(3) Le Cash burn, également appelé érosion des capitaux, correspond au temps que mettra une entreprise déficitaire à dépenser sa trésorerie, si ses pertes restent stables. Une information utile dans le monde des start-up, qui mettent souvent plusieurs années à devenir profitables. Les investisseurs qui placent leurs fonds dans ces jeunes pousses demandent souvent aux entrepreneurs quel est leur Cash burn pour estimer combien de temps leur société pourra subsister sans nouvelle levée de fonds. Plusieurs géants du Net comme Amazon ou Facebook ont travaillé à perte, utilisant le cash de leurs investisseurs pendant plusieurs années avant de devenir rentables.

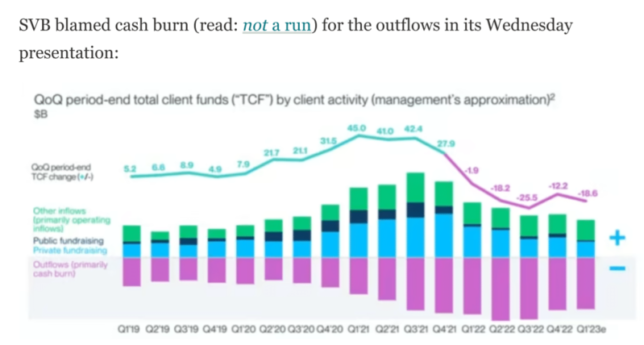

L’élément déclencheur, à l’évidence, est une consommation rapide de la trésorerie des startups technologiques.

Cela ne date pas d’hier : depuis plusieurs trimestres, SBV faisait face à des sorties de dépôts importantes. Alors qu’elles étaient jusque-là compensées par d’autres entrées (privées, publiques, opérationnelles – et probablement des fonds de private equity), le solde est rapidement devenu déficitaire dès la fin de l’année 2021:

(4)

3. Run bancaire

(5) Une ruée bancaire, panique bancaire ou course aux guichets (en anglais : bank run, deposit run, deposit run-off ; la traduction littérale « course aux dépôts » n’est pas utilisée, car cette expression a un sens contraire) est un phénomène, souvent auto-réalisateur, dans lequel un grand nombre de clients d’une banque craignent qu’elle ne devienne insolvable et en retirent leurs dépôts le plus vite possible.

Le run bancaire de SVB a surpris les marchés financiers :

(2) Silicon Valley’s business boomed as tech companies did well during the pandemic. That filled the lender’s coffers, and SVB had about $174 billion in deposits.

But in recent months, many of Silicon Valley Bank’s clients had been withdrawing money at a time when the tech sector as a whole has been suffering.

SVB said earlier this week, that in order to make good on those withdrawals, it had to sell part of its bond holdings at a steep loss of $1.8 billion. Bonds and stocks have been hammered since last year, as the Federal Reserve has raised interest rates aggressively, and SVB also noted it wanted to pare down its bond portfolio to avoid further losses.

But that announcement spooked the bank’s clients, who got worried about SVB’s viability, and then proceeded to withdraw even more money from the bank — a textbook definition of a bank run.

Nous en savons un peu plus sur les montants invraisemblables des retraits demandés :

(6) … the California Department of Financial Protection and Innovation reported that … “investors and depositors reacted by initiating withdrawals of $42 billion in deposits from the Bank on March 9, 2023, causing a run on the Bank.”

As a result of this furious drain, as of the close of business on Thursday, March 9, “the bank had a negative cash balance of approximately $958 million.”

At this point, despite attempts from the Bank, with the assistance of regulators, “to transfer collateral from various sources, the Bank did not meet its cash letter with the Federal Reserve. The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they come due, and the bank is now insolvent.”

Some context: as a reminder, SIVB had $173 billion in deposits as of Dec 31., which means that in just a few hours a historic bank run drained a quarter of the bank’s funding!

4. Effets de contagion

Particulièrement visibles ces derniers jours dans les marchés, c’est un terme qu’il convient de décliner tant ses effets sont variés et de différentes natures.

Nous en voyons trois. Le dernier est, de loin, le plus structurel et systémique.

4.1 Contagion directe

Exposition directe, dépôts auprès de SBV, modèles d’affaires similaires, conséquences immédiates…

(7) Circle, the operator of one of the world’s largest stablecoins, has said $3.3bn of its reserves are trapped in Silicon Valley Bank, triggering a fall in the value of its token as the crypto market reels from the failure of two US banks this week.

The announcement from Circle overnight on Friday prompted the company’s USDC crypto token to lose its peg to the dollar.

US exchange Coinbase said it was temporarily pausing conversions between USDC and the US dollar. Rival exchange Binance also said it would pause automatic conversions of USDC to BUSD, a stablecoin that carries the Binance branding.

Circle called for an urgent federal rescue plan for SVB.

(8) Trading in banking groups PacWest, Western Alliance and First Republic — all of which are seen to have similar depositor profiles — experienced pauses after sharp falls triggered volatility “circuit breakers”. First Republic shares ended the day off almost 15 per cent while its smaller rivals tumbled 38 per cent and 21 per cent respectively.

Shares of New York-based Signature Bank, known for its services to the cryptocurrency industry, dropped by almost a quarter.

(9) The impact is being felt beyond start-ups. Roku, the $24bn streaming hardware group that went public in 2017, disclosed on Friday that more than a quarter of its $1.9bn in cash and equivalents, about $487mn, were deposited at SVB. It said it was uncertain to what extent it would be able to recover the uninsured portion of the funds.

4.2 Contagion liée à la hausse des taux d’intérêt, à la gestion des liquidités, ALM, carry

Si l’on en croit ces statistiques bancaires, la grande majorité des banques a placé les excès de dépôts accumulés ces dernières années dans des investissements plus rentables. Mal maîtrisée – c’était visiblement le cas de SVB – cette stratégie de ‘carry’ s’avère dangereuse en cas (i) de baisse des investissements cibles et (ii) de réalisation forcée de ces derniers:

(10) The failure of Silicon Valley Bank and the sell-off in US banks that followed have highlighted the lasting dangers of a strategy many lenders used to boost profits when interest rates were low.

Starting in April 2020 and peaking two years later, nearly $4.2tn in deposits poured into US banks, according to data from the FDIC. But just 10 per cent of that ended up funding new lending. Some banks just held those new deposits in cash. But much of the money, some $2tn, was funnelled into securities, mostly bonds. Prior to the pandemic, banks had just over $4tn in securities investments. Two years later those portfolios had risen by 50 per cent.

But what is just a headwind for the nation’s largest banks could be a tornado for some smaller lenders that bet heavily on their bond portfolios. That is in large part what happened at Silicon Valley Bank, which accumulated $15bn in losses in its bond portfolio, only slightly less than the overall worth of the bank.

PacWest, which is based in Beverly Hills, California, for example, has accumulated $1bn in losses in its bond portfolio, enough to wipe out more than a quarter of its $4bn in equity. Shares of PacWest have plunged 50 per cent in the past week.

4.3 Contagion réglementaire, absence d’assurance

Le cas de SVB fait apparaître d’autres questions bien plus structurelles relatives à la réglementation, la supervision bancaire, aux ratios de liquidité ou à la gestion des crises bancaires. Elles renvoient directement aux crises bancaires précédentes:

(11) If you think back to the Great Financial Crisis, one of the big things you’ll remember is that for the first time in living memory, major banks were subject to liquidity runs… You might also remember that in the aftermath of that crisis, regulators assured us all that the rules had been changed to prevent that sort of thing.

So what’s happened with Silicon Valley Bank (and Silvergate) then? You’re going to laugh.

… So the Fed adopted a rule under which only the very largest international banks were subject to the full Basel NSFR requirements (several of those large banks are actually holding companies for foreign institutions). It adopted a second tier, under which the ratio only had to be 85%, and a third tier where it was calibrated to 70%. And even then, the majority of US banks are not required to follow the NSFR or LCR standards at all.

Despite being the 16th largest bank in the US by balance-sheet size, SVB was apparently not subject to the “no more Dexias, no more HBOSes” regulation. The reason, as implied in the 10-K disclosure above, seems to be that a bank is only required to follow the NSFR and LCR rules if they have a certain amount of “short term wholesale funding”, and SVB’s liability side was dominated by deposits from corporate customers.

(12) Silicon Valley start-ups are scrambling to pay staff and identify sources of back-up funding after regulators stepped in and shut down Silicon Valley Bank on Friday morning, stranding deposits that serve as the lifeblood of many early-stage technology companies.

“There’s a lot of money that flows through those bank accounts every day that suddenly is not moving. There will be big consequences for the whole ecosystem. Employees getting paid, suppliers getting paid, financing [rounds] closing.”

Deposits of up to $250,000 are federally insured but the majority of SVB clients fall outside that threshold. The bank reported at the end of last year that $151bn of its $173bn in total domestic deposits was uninsured. The FDIC said clients will get access to insured deposits by Monday morning, while uninsured depositors will get an advanced dividend and a receivership certificate for anything above that sum.

5. Et maintenant? Bailout ou non? Haircut?

(1) The FDIC said those with insured deposits with SVB, typically up to $250,000, would be able to access their money by no later than Monday.

The fate of those with deposits at SVB that exceed insurance limits is less certain, however, with the FDIC saying they will receive an “advance dividend” for a portion of their funds along with “certificates” accounting for their uninsured funds.

The regulator did not spell out what that would entail for these uninsured depositors. Investors will also continue to monitor for any further impact on other banks. The Treasury Department said Secretary Janet Yellen discussed the situation at a meeting she convened with financial regulators.

Propositions :

– L’élément central de la faillite SVB est une bulle des investissements réels (ici dans la technologie, mais nous pouvons imaginer que d’autres secteurs d’activités ‘hype’ sont concernés) rendue possible par les politiques de taux irréelles de ces dernières années et leur accélération durant la pandémie.

Ce gérant voyait juste :

(2) As a venture capital investment bubble began to inflate in early 2021, Nate Koppikar, a partner at hedge fund Orso Partners, began studying SVB as a way to bet against the industry at large.

“The problem with the business model is that when capital dries up, the deposits flee,” said Koppikar. “It was one of the best ways to short the tech bubble. The fact this bank failed shows that the bubble has burst.”

– Les failles de stabilité financière sont l’expression d’une normalisation financière forcée. Même si leur timing est difficile à prévoir, SVB s’inscrit dans une suite logique d’événements financiers dont la crise des Gilts anglais est une autre illustration ;

– Parmi les sources de contagion évoquées dans ce billet, les plus sérieuses nous semblent être les plus structurelles, en particulier celles qui cautionnent des stratégies industrielles de ‘carry’, ou qui consisteraient à rembourser des clients qui ont volontairement renoncé à assurer leurs dépôts ;

– Il s’agit d’un problème d’aléa moral classique souvent commenté dans ce blog. A force d’être mutualisés, les risques sont amplifiés par les acteurs financiers ;

– Le maintien de la stabilité financière, un des objectifs des banques centrales, a souvent servi de munition monétaire. S’il est une erreur de politique publique, c’est probablement à cet endroit qu’elle se trouve ;

– La faillite de SVB est une nouvelle tentative de revalorisation des risques de la part du marché: les autorités publiques seraient très inspirées de laisser le marché mettre un prix sur cette accumulation de risques…

– …à commencer par l’industrie du private equity qui, nous semble-t-il, a été bien prompte à solliciter un nouveau bailout en provoquant le run bancaire.

Pile je gagne, face tu perds…

Addendum:

Ce billet a été rédigé entre samedi 11 et dimanche 12 mars 2023. Nous apprenions dans la nuit de dimanche à lundi la décision des autorités de garantir l’intégralité des dépôts:

(13) The Fed is acting as it should as a provider of liquidity to all comers. But it’s going further and offering one-year loans to banks against collateral of Treasurys and other fixedincome assets. The Fed will value these assets at par, which means banks don’t have to sell their assets at a loss. The Fed is essentially guaranteeing bank assets that are taking losses because banks took duration risk that Fed policies encouraged. This too is a bailout.

Perhaps this will contain any Monday market mayhem, but if it doesn’t our guess is that the Treasury, FDIC and Fed will look to guarantee uninsured deposits across the banking system. The Fed will want to avoid institutional blame for financial damage, and President Biden will do anything to avoid letting a financial panic affect the overall economy as he prepares to run for a second term next year.

Et cette conclusion du WSJ que nous n’aurions décidément pas mieux pu formuler. Si nos clefs de lecture sont correctes, c’est le meilleur moyen, à ce stade, de préparer le prochain épisode systémique:

You can’t run the most reckless monetary and fiscal experiment in history without the bill eventually coming due. The first invoice arrived as inflation. The second has come as a financial panic, with economic damage that may not end with Silicon Valley Bank.

Jacques

Sources:

(1) A Silicon Valley lender collapsed after a run on the bank. Here’s what to know, npr.org, March 10 2023

(2) Silicon Valley Bank: the spectacular unravelling of the tech industry’s banker, FT, March 12 2023

(3) ‘Cash burn’, le journal du net

(4) Silicon Valley Tank(s), FT Alphaville, March 9 2023

(5) Run bancaire, wikipedia

(6) Record Bank Run Drained A Quarter, Or $42BN, Of SVB’s Deposits In Hours, Zero Hedge, March 11 2023

(7) Crypto group Circle admits $3.3bn exposure to failed Silicon Valley Bank, FT, March 11 2023

(8) California bank failure shakes global financial stocks, FT, March 10 2023

(9) Silicon Valley Bank shutdown leaves start-ups anxious about their funds, FT, March 10, 2023

(10) Cheap deposits have become a painful pandemic hangover for US banks, FT, March 11, 2023

(11) Silicon Valley Bank is a very American mess, FT, March 11, 2023

(12) Silicon Valley Bank shutdown leaves start-ups anxious about their funds, FT, March 10, 2023

(13) The Silicon Valley Bank Bailout, WSJ, March 13, 2023