Sometimes economic and market developments combine and force us to focus our interventions.

As foreseen some time ago, things seem to speed up in terms of credit deleveraging. The issue looks highly relevant from a macro standpoint as it probably highlights our ‘risk repricing scenario’.

Let us revert to Canada, which seems to stand at the forefront of some of the most recent developments. The Canadian economy actually sits at the crossroad of commodities and real estate as income generating levers and credit sensitive variables. Some multi-sigma events attracted our attention of late, here is a follow-up of their possible warning signals.

Likewise, note the central role of financial stability when it comes to systemic risks. That’s is precisely where we would expect Central Banks to position themselves in a world of cheap public promises. Interestingly enough, the double message of the latest FOMC meeting – interest rate hike and balance sheet normalisation – has not been understood under such lenses. We believe it’s a matter of time.

Back to Canada where the deleveraging process is well underway.

Please consider ‘ Bank of Canada Cites Household Debt, Real-Estate Prices as Top Stability Risks’ by the Wall Street Journal:

(bold ours)

| Rising Canadian household debt and frothy real-estate markets are the main concerns for financial stability in the country, with conditions exacerbated in the past six months by significant house-price gains in Toronto and the surrounding area, the Bank of Canada said Thursday.

On eight occasions starting in 2008, federal and provincial authorities in Canada have introduced measures to tamp down housing exuberance. But housing has been a crucial growth engine for the country, as TD Bank estimates that 40% of Canadian economic output since 2014 is tied to real estate. In Toronto, price growth “has been too fast for normal market activities,” the central bank said. It said speculation and what it calls “extrapolative expectations”—or a widespread belief among buyers and investors that house prices will continue to move upward—are driving the Toronto market. When combined with elevated levels of debt, “this activity can be destabilizing.” Recent data suggest Toronto-area housing activity could be slowing, amid non-rate tools to contain exuberance. Home sales activity in Toronto sank 20% in May, according to the Toronto Real Estate Board. |

Let us dig into this last set of data.

The Wall Street Journal also comments: ‘Canada Existing Home Sales Plunge in May on Ontario Rules’

| Sales of existing homes in Canada fell sharply in May from the prior month, recording the biggest decline in nearly five years, reflecting measures introduced in the province of Ontario that appear to have “squelched” speculation and rapid price gains in the Toronto market.

|

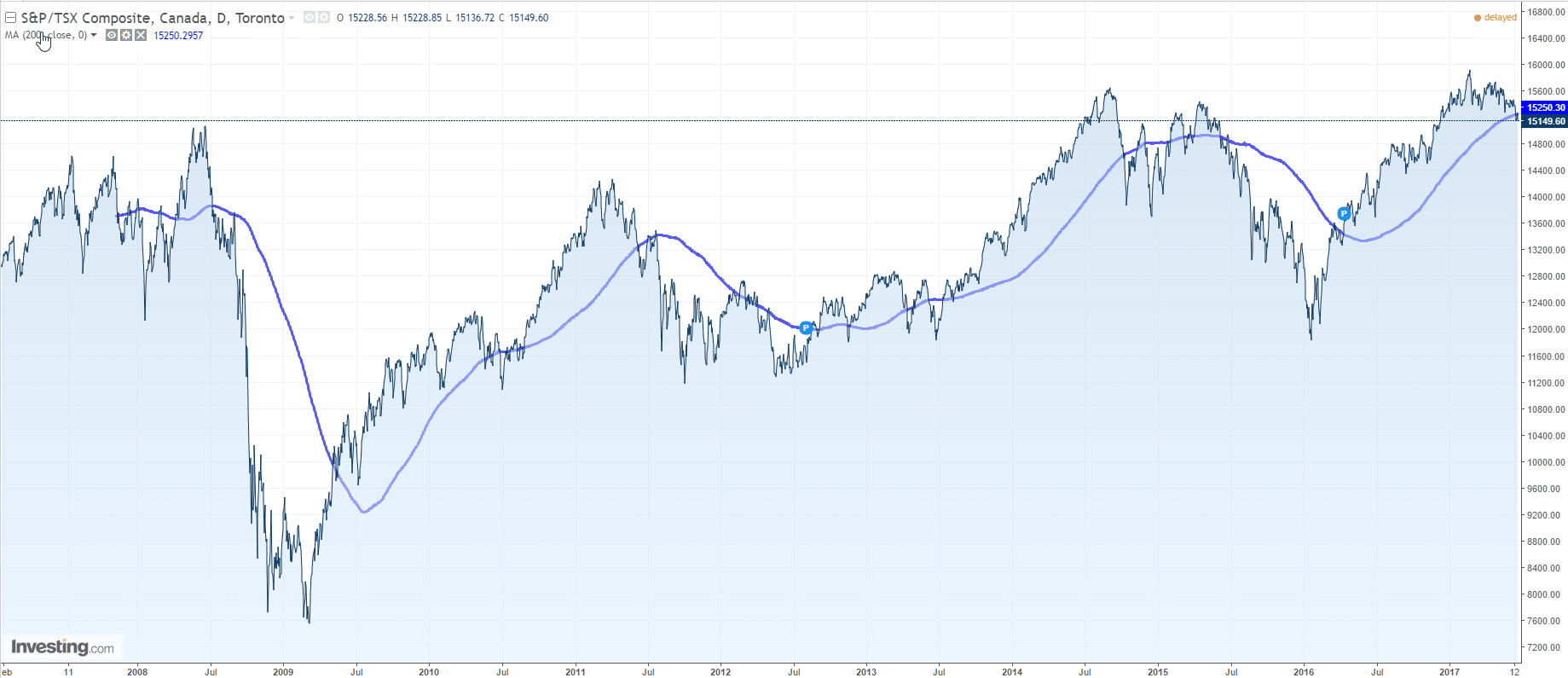

What about the equity market ?

This nice technical picture was suggested by Sober Look in a recent Daily Shot. Here’s a larger perspective from Investing.com:

Jacques