China and the Fed

Our macro-credit radar is flashing red again.

Interestingly enough, this happens at the crossroad of well-known macro-financial dimensions discussed in this blog: emerging growth, credit as a macro lever, public authorities and financial stability.

Also of interest, it happens hours after the latest Federal Reserve statement and weeks before an important congress of the Chinese Communist party.

Please consider “S&P Cuts China’s Credit Rating, Citing Risk From Debt Growth” by Bloomberg:

(emphasis added)

“Global Ratings cut China’s sovereign credit rating for the first time since 1999, citing the risks from soaring debt, and revised its outlook to stable from negative.The sovereign rating was cut by one step, to A+ from AA-, the company said in a statement late Thursday. The analysts also lowered their rating on three foreign banks that primarily operate in China, saying HSBC China, Hang Seng China and DBS Bank China Ltd. would be unlikely to avoid default should the nation default on its sovereign debt.

“China’s prolonged period of strong credit growth has increased its economic and financial risks,““Although this credit growth had contributed to strong real gross domestic product growth and higher asset prices, we believe it has also diminished financial stability to some extent.

“The downgrade, the second by a major ratings company this year, represents ebbing international confidence that China can strike a balance between maintaining economic growth and cleaning up its financial sector.”

|

“The world’s second-biggest economy is forecast to slow after a robust first half, when it started the year with the first back-to-back quarterly acceleration in seven years, then surprised economists by matching that 6.9 percent expansion again in the second quarter. Economists surveyed by Bloomberg this month project growth will remain above 6 percent through 2019.”

|

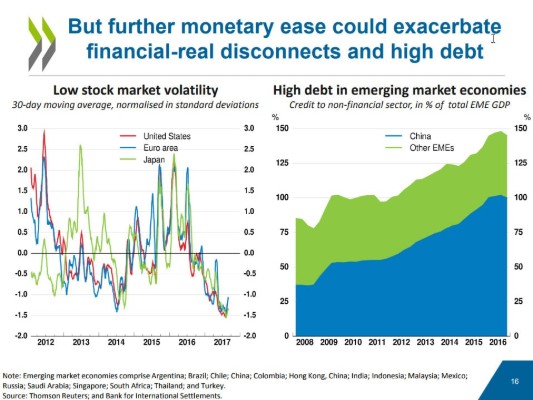

Real-financial disconnects driven by credit growth

From the statement:

(our emphasis)

“The downgrade reflects our assessment that a prolonged period of strong credit growth has increased China’s economic and financial risks. Since 2009, claims by depository institutions on the resident nongovernment sector have increased rapidly. The increases have often been above the rate of income growth. Although this credit growth had contributed to strong real GDP growth and higher asset prices, we believe it has also diminished financial stability to some extent.”

|

“The recent intensification of government efforts to rein in corporate leverage could stabilize the trend of financial risk in the medium term. However, we foresee that credit growth in the next two to three years will remain at levels that will increase financial risks gradually.”

|

Global impacts

And the outlook:

“We may raise our ratings on China if credit growth slows significantly and is sustained well below the current rates while maintaining real GDP growth at healthy levels. In this scenario, we believe risks to financial stability and medium-term growth prospects will lessen to lift sovereign credit support. A downgrade could ensue if we see a higher likelihood that China will ease its efforts to stem growing financial risk and allow credit growth to accelerate to support economic growth. We expect such a trend to weaken the Chinese economy’s resilience to shocks, limit the government’s policy options, and increase the likelihood of a sharper decline in the trend growth rate.”

|

As a reminder, the OECD rose a very similar flag in its latest interim economic outlook :

Source: OECD

These developments are usually considered as ‘international’ from an American or European standpoint.

As the 2015 Chinese turmoil and its subsequent events demonstrated however, they can have significant global impacts, which may interfere with local policy responses. An issue that an almost hidden, tiny little passage of the latest FOMC statement kindly reminded us:

“This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.”

Precisely, this looks like an additional bold international reading.

Jacques

A blog about finance