We stick to our previous statements: the rise in interest rates is less related to some sudden expectations of growth than a fierce repricing of credit risks.

This happens – we believe – on the back of a forced and global exit strategy. Let us dig a bit into this proposition by looking at the champion of unconventional policies: Japan.

Please consider ‘Bank of Japan: Backward guidance’.

How long will the BoJ manage to stick to its ‘comprehensive assessment’ pledge to keep the 10Y JGB yield below zero ?

Tough job …

Along the same line: how long will the SNB manage to stick to its ‘implicit peg’ of 1.08 CHF vs. EUR ?

If not – as we believe – how far could the CHF strengthen and what would this mean ? Propositions below.

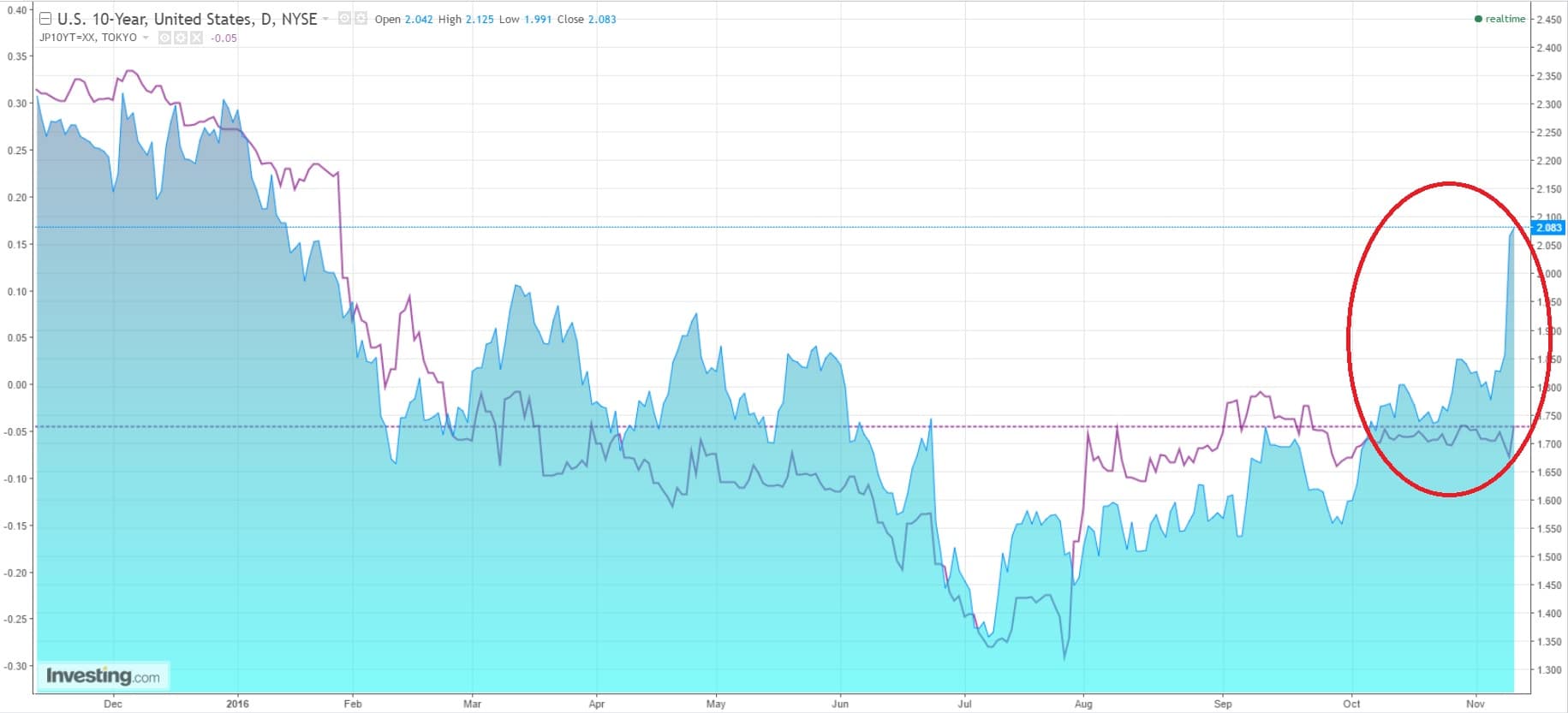

Source: investing.com

We suggest:

– The US presidential outcome is not a game changer but a game booster: the trends above were already in place prior to the election. Expect them to unfold ;

– Systemic and financial risks remain extremely high. As for the Brexit, central banks had to operate massively ;

– For how long ?

Expect further volatility down the road as underlying risks are materializing and central banks are still forced to exit.

Stay tuned, more to come.

Jacques

Good Evening Jacques,

“– The US presidential outcome is not a game changer but a game booster: the trends above were already in place prior to the election. Expect them to unfold ;”

Completely agree. Reflation all around. Also, earlier this year, we changed our deflationary view held for nearly 10 years to much more neutral, as being long bonds finally became the accepted (and very crowded) view. Metals are showing us the way. For the first stage of reflation, I’d say be long equities (rising earnings). What’s your favourite trae?

Thank you for sharing André,

I’m not much on the reflationary camp I’m afraid.

As mentioned in the post I believe that one should not mix up credit repricing with a virtuous reflationary comeback. Appealing but I just fail to see it.

As the election dust settle I think that the underlying economic pattern will re-emerge, i.e. a very soft one. In the first place I expect interest rates to be a drag on leverage, which as you know is sky high.

As far as my topics of interests (and risks!) are concerned, I would focus on the negative impact of an interest rate shock on various carry trades: credit, oil (which I believe is a big part of the reflation call), emerging markets and currencies, the cost of debt, capital flows and trade. Not to forget the level of activism of central banks, which – I believe – is increasingly tested by the market.

Rightly so.

Read you soon,

Jacques