Further market developments following the flow of taper guidance issued recently … this time by the Bank of England.

As a reminder, the BoE issued some rather unusual guidance yesterday.

As the FT’s suggests in “Hawkish BoE spurs markets to revise rate expectations”, the move could work as a kind of market test ahead of the next Monetary Policy Committee:

(emphasis added)

“The Bank of England has issued its strongest guidance in a decade that it is poised to raise interest rates, setting the stage for a nail-biting decision at the November meeting of the Monetary Policy Committee.” “This guidance on rates is unusual from the BoE and suggests the committee is seeking to test financial markets’ likely response to a quarter point rate rise from the current low of 0.25 per cent at the November meeting.“It also puts the BoE on the same course as two of the world’s other major central banks, the US Federal Reserve and the European Central Bank, for a simultaneous tightening of crisis-era easy money policies before the end of the year.“ ”With the European Central Bank signalling that it would decide in October how to phase out its €60bn-per-month stimulus, yesterday’s announcements set the stage for a fourth quarter where all three banks could move to normalise policy after months — in some cases years — of inaction.“ ”Most economists rushed to change their expectations of interest rate rises in the wake of the BoE’s words.” |

Sounds familiar?

It should : FX markets look particularly sensitive to such expectations, in particular when they are triggered by bold and insisting communication campaigns.

Please consider “The Pound Surges to a Post-Brexit High” by Bloomberg:

“The pound climbed to the highest level against the dollar since just after the Brexit vote and U.K. government bonds tumbled as Bank of England policy maker Gertjan Vlieghe stoked speculation of an interest-rate increase within months.” |

Source: Bloomberg

| “The evolution of the data is increasingly suggesting that we are approaching the moment when the bank rate may need to rise,” Vlieghe said in a speech at the Society of Business Economists in London. If the economy continues apace, “the appropriate time for a rise in the bank rate might be as early as in the coming months.” |

“If the economy continues apace”.

Which pace exactly ?

Source: IHS Markit

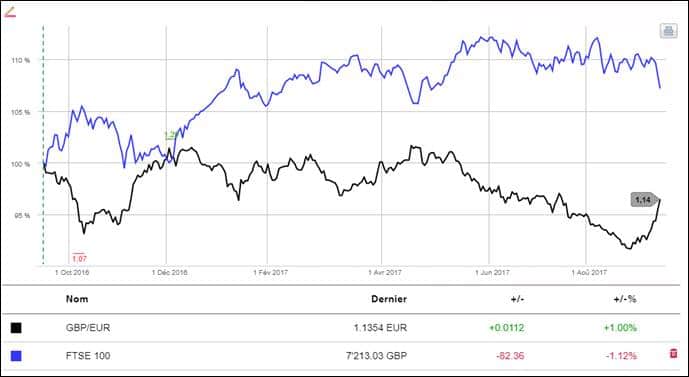

What about the equity market? The chart below looks self-explanatory …

And the same concluding question: if the economy fails to be apace, why does the BoE ignite a surprising ‘taper guidance’ strategy ?

Some hints :

Hint 1: UK inflation indicates that the FX measures taken after the Brexit have gone too far. They could actually conflict with the mandate of the BoE ;

Hint 2: if the BoE fails to synchronize its guidance with the communication of the Fed or the ECB, point 1 could get even worse ;

Hint 3: oil prices have surged more than 15% since mid-June, interest rates expectations have reacted accordingly in the US.

More to come, the normalisation path looks decidedly crowded these days.

Jacques